Pendle Finance (PENDLE): Bear Market Investment Thesis

1. Executive Summary

Verdict: Cautious accumulation. Not a conviction buy at current prices, but a protocol worth owning a position in ahead of the next cycle — with the understanding that further drawdown is possible and timing is uncertain.

Pendle Finance is not a broken protocol. It is a cyclical one. TVL has collapsed 80% from its October 2025 peak of $11b to $2.31b today, trading volume is near zero, and fee revenue has compressed to $1.15m per month. On present metrics alone, the investment case is weak.

However, the data also reveals a protocol with demonstrated peak capacity, a net-positive earnings profile even at trough, and — most strikingly — sustained voluntary commitment from holders who continue to lock tokens through the drawdown. At $1.23, PENDLE trades near its pre-breakout 2023 levels, before the market had witnessed its $11b TVL or $7-8m monthly fee capacity. That asymmetry is the core of this thesis.

2. What Pendle Actually Does

Pendle Finance is a DeFi yield tokenization protocol that splits yield-bearing assets into two components: Principal Tokens (PT) and Yield Tokens (YT).

- PT holders receive a fixed, predetermined yield at maturity — a conservative position suited for capital preservation.

- YT holders take leveraged exposure to the variable yield stream, a speculative position that performs best in high-yield, high-activity environments.

This structural duality is central to the bear market question. In theory, fixed-yield instruments should attract risk-averse capital during downturns. In practice, the answer is more complicated — and the data tells that story clearly.

3. The Bear Market Context

As of February 2026, the crypto market is navigating a prolonged risk-off environment. Following the cycle peak in late 2024 and an aggressive rally into October 2025, total crypto market capitalization has contracted sharply. Bitcoin dominance has risen as capital rotates out of altcoins and DeFi into perceived safety. Sentiment indicators, on-chain activity, and DEX volumes across the board reflect a market in consolidation at best, and continued distribution at worst.

For yield protocols specifically, this environment creates a structural paradox. Bear markets theoretically favor fixed-yield instruments — investors seeking capital preservation over speculation should gravitate toward PT-style positions. However, the same bear market suppresses the underlying yield rates on assets like stETH, sUSDe, and other yield-bearing tokens that Pendle pools are built on. Lower underlying yields mean less attractive PT fixed rates, which means less reason to deploy capital into Pendle in the first place.

4. On-Chain Data: What the Numbers Say

4.1 Is Capital Leaving?

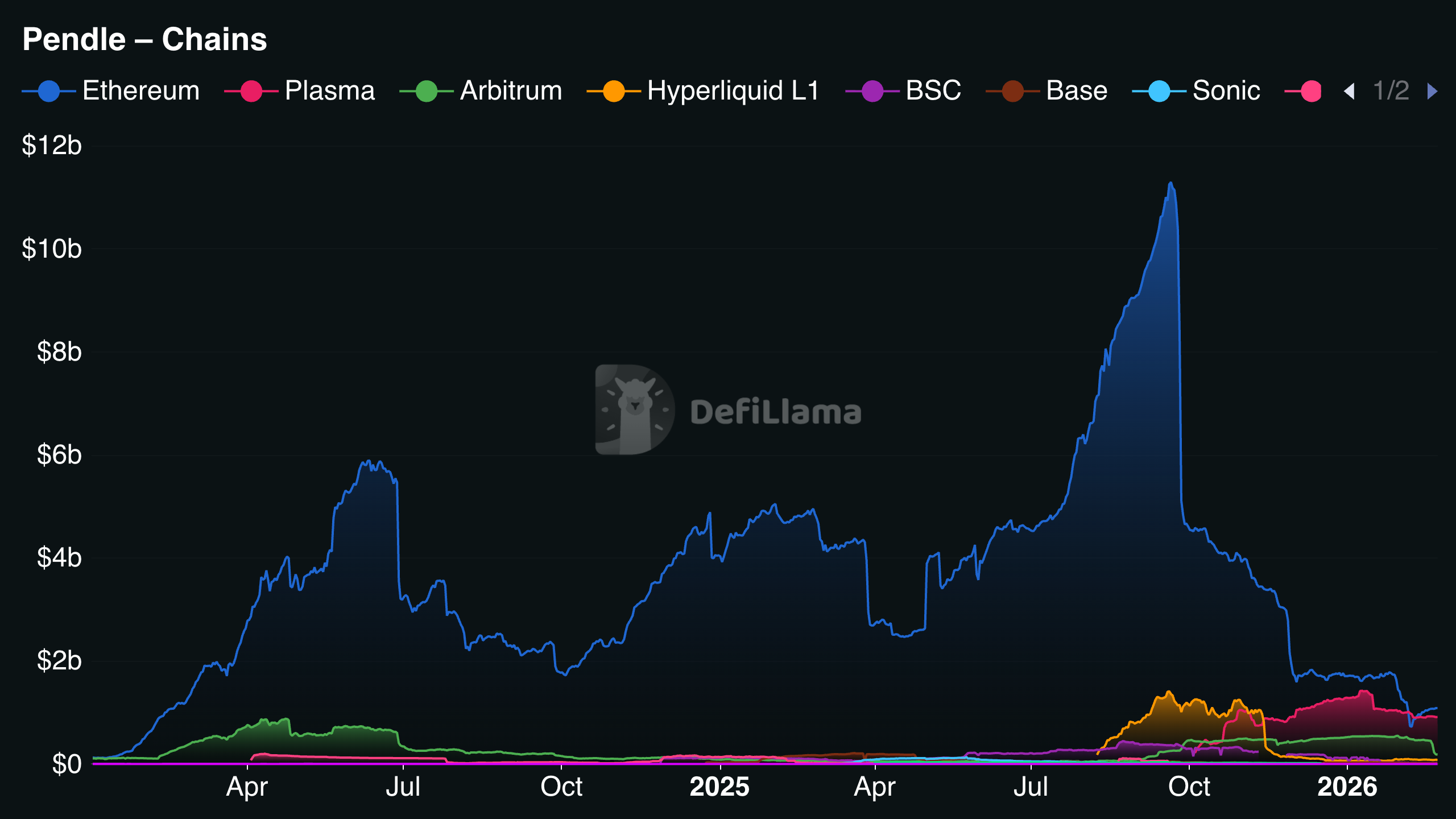

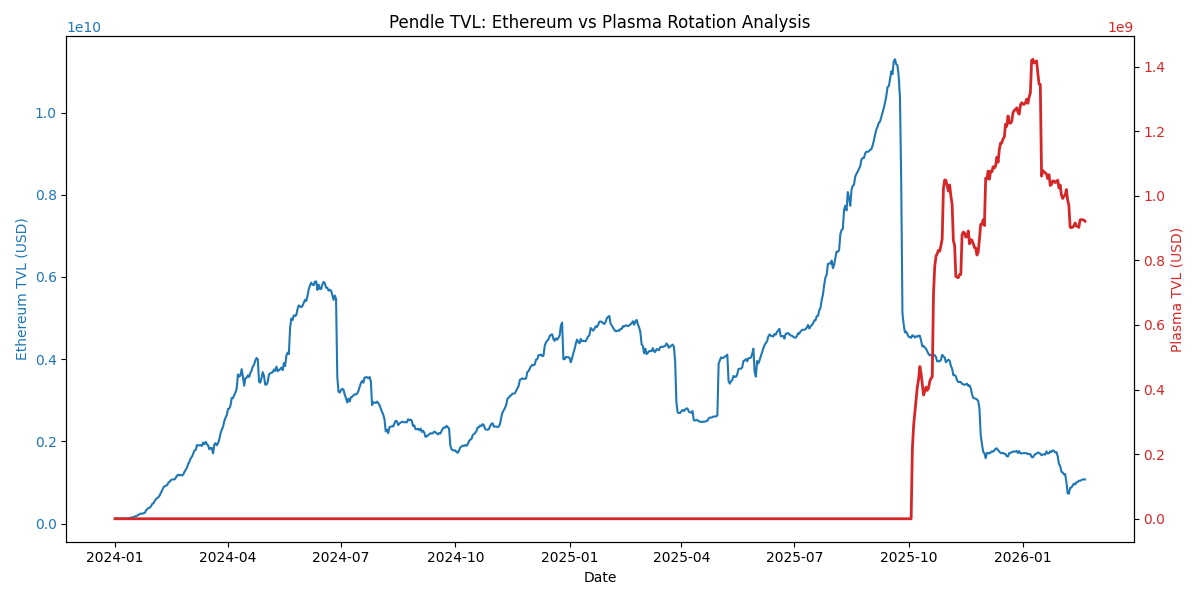

The answer is unambiguous. Pendle’s total TVL peaked at approximately $11b in October 2025 before collapsing to $2.31b as of February 20, 2026 — an 80% drawdown in roughly four months. This was not a slow bleed but a cliff-shaped decline, suggesting a sharp sentiment shift rather than organic rotation out.

The chain-level breakdown adds nuance. Ethereum, historically Pendle’s dominant chain, fell from roughly $11b at peak to $1.07b today. However, a rotation into Plasma emerged approximately two weeks after Ethereum’s September 2025 peak — a lag that strongly suggests capital migration rather than new entrants. Plasma itself peaked at $1.4b on January 9, 2026, and has since declined. There is currently no new chain absorbing outflows. The rotation story is exhausted.

4.2 Is the Protocol Still Making Money?

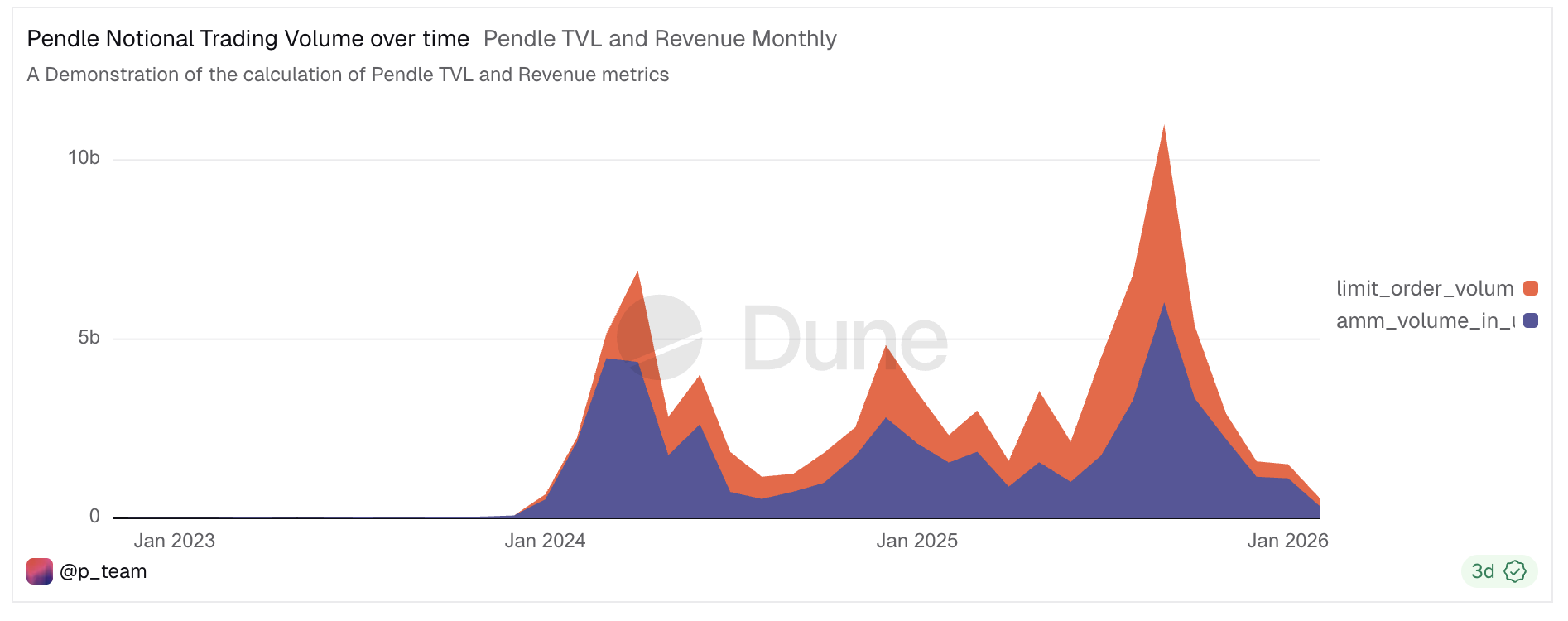

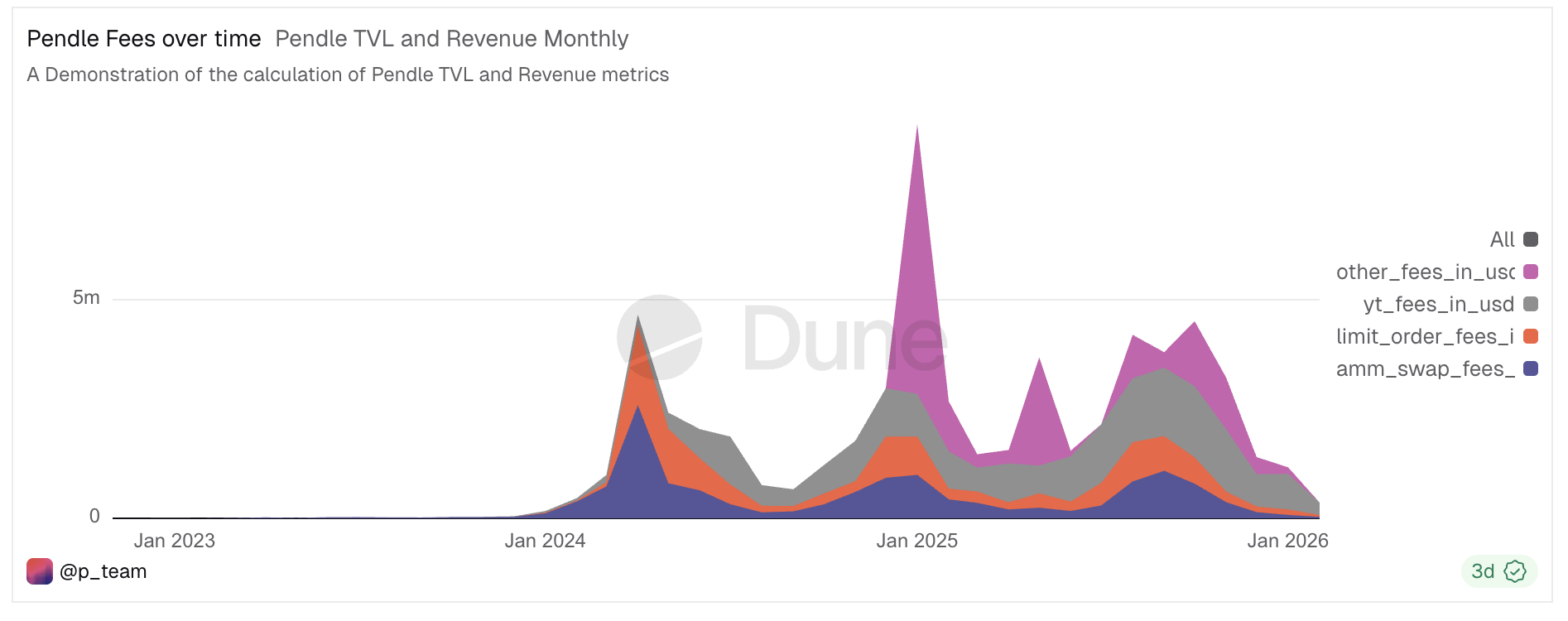

Trading volume tells a stark story. Notional trading volume, which peaked at over $10b in October 2025, has collapsed to near zero entering 2026. This directly flows into fee revenue.

| Metric | Value |

|---|---|

| Last Month Total Fees | $1,167,019 |

| Last Month Total Revenue | $1,151,500 |

| Annualized Revenue (implied) | ~$13.8m |

| Market Cap | $203.62m |

| Fully Diluted Valuation (FDV) | $347.26m |

| Price / Revenue (MCap) | ~20x |

| Price / Revenue (FDV) | ~33x |

| Annualized Earnings | $5.84m |

| Annualized Incentives | $4.52m |

One anomaly worth flagging: the fee chart shows an unusual spike in ‘other fees’ around January 2025, briefly pushing monthly fees to $7-8m. This appears to be a one-time event — likely a large pool expiration or fee structure change — and should not be treated as representative of baseline revenue capacity.

Notably, despite trough-level activity, Pendle remains net profitable. Annualized earnings of $5.84m against annualized incentive spend of $4.52m means the protocol is not subsidizing itself to stay alive. That matters.

4.3 Who Is Still Here?

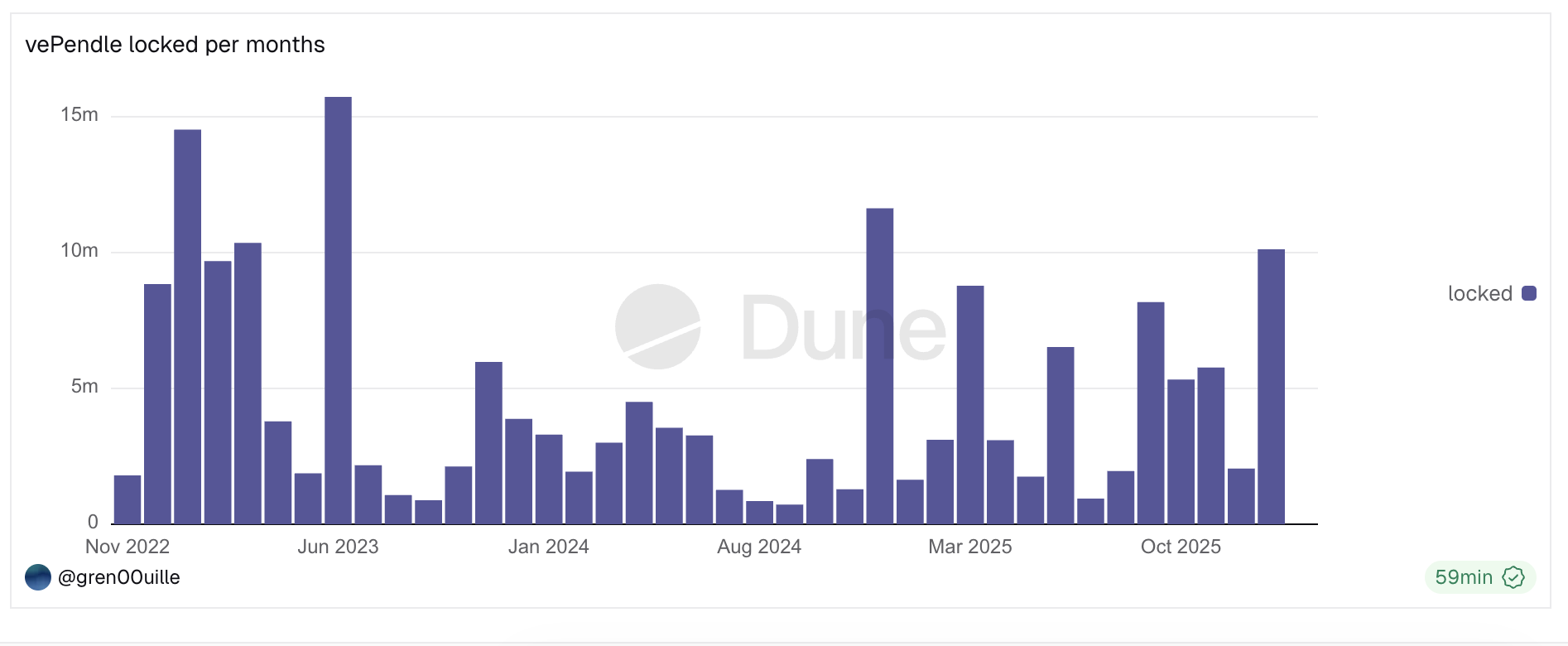

Despite the activity collapse, 58.7% of PENDLE’s market cap — approximately $119.5m — remains staked as vePENDLE. Monthly lock flow data reveals this is not captive capital. Net vePENDLE flow has been positive in 9 of the last 12 months, with cumulative locked supply growing from approximately 54m to 68m tokens through the bear market. January 2026 alone saw 10.1m tokens freshly locked — right as TVL was collapsing.

The one exception is February 2026, which shows near-zero new locking and 1.38m withdrawn. At only 20 days in, it is too early to call this a trend — but it warrants monitoring in the months ahead.

5. The Structural Argument

The bear case for Pendle is straightforward: activity has collapsed, revenue is at trough, the token is not cheap on current fundamentals, and the internal rotation story — Ethereum to Plasma — has already run its course. On present numbers alone, the investment case is weak.

But present numbers are not the whole story.

Pendle’s core value proposition — yield tokenization — is not broken. It is dormant. The protocol demonstrated at peak that it can attract $11b in TVL and generate tens of millions in monthly fees when market conditions are favorable. That capacity does not disappear in a bear market. It waits.

More importantly, fixed-yield instruments historically become more attractive as a cycle matures into recovery. As underlying yields on stETH, sUSDe, and comparable assets begin recovering with returning market activity, PT rates become compelling again — first to institutional and risk-averse capital, then to the broader market. Pendle is structurally positioned to be an early beneficiary of any DeFi volume recovery, not a laggard.

Analysis of monthly vePENDLE lock flows shows net positive staking in 9 of the last 12 months, with cumulative locked supply growing from approximately 54m to 68m tokens despite the bear market. January 2026 alone saw 10.1m tokens freshly locked. This is not captive capital — it is active accumulation.

6. Key Risks

6.1 No Revenue Floor

Pendle’s business model is entirely activity-dependent. Unlike lending protocols that generate interest continuously, or bridges that capture fees on every transfer, Pendle only earns when people actively trade PT and YT. If the bear market extends another 12-18 months, there is no minimum viable revenue to sustain token value. The protocol survives, but the token bleeds.

6.2 Underlying Yield Compression

Pendle’s pool attractiveness is directly tied to the yield rates of its underlying assets — stETH, sUSDe, and similar instruments. In a prolonged risk-off environment, these yields compress as demand for leverage collapses. Lower underlying yields mean less attractive PT fixed rates, which means less reason for capital to enter Pendle pools regardless of market sentiment toward the protocol itself.

6.3 February 2026 Lock Activity

The vePENDLE monthly flow data shows near-zero new locking in February 2026, with 1.38m tokens withdrawn and essentially nothing entering. While it is too early to call this a trend — only 20 days of data — it warrants monitoring. If March and April show similar patterns, the conviction narrative weakens materially and selling pressure from unlocks becomes a real overhang.

7. Verdict & Catalyst Watch

Pendle is not a broken protocol. It is a cyclical one. The same mechanism that made it irrelevant in the 2022-2023 bear market is also what made it one of the standout performers when conditions improved. The current environment is a near-identical setup.

At $1.23, PENDLE is trading near its pre-breakout 2023 levels — a price at which the market had not yet witnessed Pendle’s capacity to absorb $11b in TVL or generate $7-8m in monthly fees. Buying at these levels means paying 2023 prices for a protocol with a demonstrated 2025 track record. That asymmetry is real.

However, the valuation is not unambiguously cheap. At a 20x Price/Revenue multiple on trough earnings, the market is already pricing in some degree of recovery. The token is not distressed — it is waiting. And waiting has a cost, particularly if the bear market extends further or if February’s near-zero lock activity marks the beginning of a conviction breakdown among core holders.

The investment case for Pendle therefore rests on a single core belief: that DeFi activity recovers within a reasonable time horizon and that Pendle retains its dominant position in yield tokenization when it does. The on-chain data — specifically the sustained vePENDLE lock flows through the drawdown — suggests the market’s most informed participants share that belief.

Watch for these catalysts:

- A sustained recovery in DEX volumes across DeFi broadly.

- New high-profile pool launches on Pendle, particularly on emerging chains.

- A reversal in the February 2026 lock flow trend.

- Any meaningful uptick in underlying LST and stablecoin yields that would make PT rates attractive again.

VERDICT: CAUTIOUS ACCUMULATION

Not a conviction buy at current prices, but a protocol worth owning a position in ahead of the next cycle — with the understanding that further drawdown is possible and timeline is uncertain.

Note: data (TVL, token price, etc) updated to 20 Feb 2026

Data Sources:

- DefiLlama (TVL, protocol metrics)

- Dune Analytics — @p_team (fees, volume, vePENDLE revenue)

- @gren0Ouille (vePENDLE lock flows)

- CoinMarketCap